Nice to Know: How to Uncomplicate Your Estate Plan.

Let’s get the hard part out of the way. The truth – you are going to die. I’ve done some research, and it turns out that statement applies to 100% of the current population. The reality – none of us spends much time thinking about it until we a) are hospitalized, b) are elderly, or c) lose a close friend or family member. And that is ok. But -- you know what they say about failing to plan!

Another truth – everyone who has reached adulthood and has accumulated any means at all and/or has children should have an estate plan. For most people, this means an Advance Directive (who will make medical decisions for me if I can’t, with some instructions on what to do in certain situations), a Power of Attorney (who will handle my business affairs if I cannot), and a Last Will & Testament (these days we just call it a Will). Those with significant means or minor children should consider a Trust, but that is another topic for another day.

To make your estate plan a lot simpler, you need to know about three things. Most people are familiar with the first two. But not many are aware of the third.

First, your banker can tell you about POD, which stands for Payable on Death. By designating your account as a POD account, you are simply saying that “upon my death, I give this account to . . . (fill in the blank). Until then, you have complete access, control, and confidentiality.

Second, your financial advisor will explain what is meant by designated and contingent beneficiaries. In general, brokerage accounts and retirement accounts are handled pursuant to a contract you sign when you open the account and that contract will include a Designation of Beneficiary(ies). This designation will often contain an opportunity to specify Contingent Beneficiaries, meaning if a beneficiary predeceases you, then you give it to someone else. For instance, you designate your spouse, but if your spouse predeceases you, then to your children – or grandchildren – or whomever you wish. It is all covered by contract, NOT by Will, and is not subject to probate. I’ve handled a number of cases over the years where someone thought that their Will trumped the beneficiary designation of their retirement account and their heirs were both surprised and disappointed to find out otherwise.

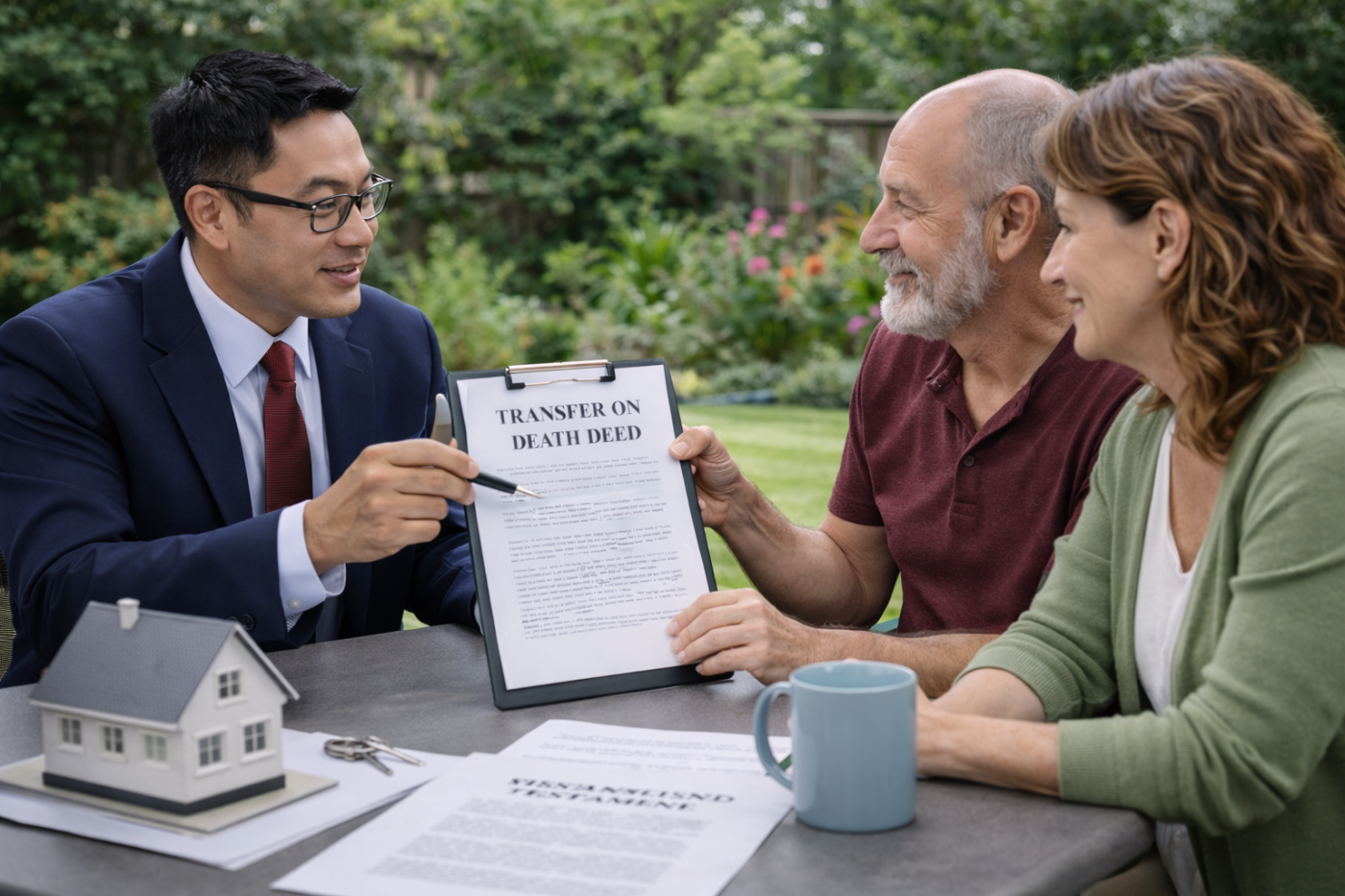

Third – and for many this is the surprise that is “nice to know” -- you can dispose of your home or other real estate immediately upon your death rather than having it tied up in probate for a year. This is done by use of a Transfer on Death Deed. This was a gift from the Indiana legislature in 2009 (pretty recent as far as legal matters go). The recording of a TOD deed does not have any current impact. You can still have a mortgage. You can borrow against the property. You can use the real estate any way you want. You can even sell it later if you choose to do so (in which case the deed is null and void and you do not “owe” anything to the grantee on the deed).

Using a TOD deed also has some pretty significant tax advantages. If you give away your home during your lifetime (perhaps to a child or grandchild), they receive your tax basis. Meaning if you paid $25,000 for your home a long time ago, and today it is worth a LOT more, your grantee will be taxed on the difference between your original cost and the sales price when they sell. One of the last great “loopholes” in the tax code is the receipt of a “stepped-up basis” in real estate when it passes upon death. By using a TOD deed, your loved ones would only pay tax on the difference between the property’s value at your date of death and the ultimate sales price, not the appreciation during your lifetime, potentially saving them tens of thousands of dollars in taxes.

One important note – a TOD deed MUST be recorded prior to the death of the Grantor. If not, it is void by statute. I recently handled a legal malpractice case against a lawyer who prepared a TOD deed for an ailing, elderly woman who signed the deed in contemplation of her impending death. She lived another three months, but the lawyer never got around to recording the deed. Sloppy work. The daughter who was to receive the mother’s residence had taken off two years of her life, lived in mother’s home as a caregiver, and was to receive the residence as her own. Instead, she had to divide it with six other siblings.

Finally, by removing that real estate from your probate estate, you eliminate significant expense from the probate process and often shorten the time to probate your estate. In some cases, using POD accounts and TOD deed(s) may completely eliminate the need for probate.

Of course, this is general information. When it comes to your personal estate plan, you will always be well served to discuss the details of your situation with a seasoned attorney.

Need an attorney to help with your Estate Plan? Why not call a Nice attorney? We’re here to help whenever you are ready to plan.